Are You Ready to Witness the Future of Data Security?

Platform

Resources

©2026 QuNu Labs Private Limited, All Rights Reserved.

India's financial system is going quiet. Not shrinking, going quiet.

The branch visit, the banking portal, the separate app login: These are giving way to banking that lives inside the platforms people already use. You pay, borrow, verify, and invest without ever feeling like you left the experience you were in. The bank has not disappeared. It has become the trusted, unseen engine running underneath. This is invisible banking, and India is one of the places where it is moving fastest.

Invisible banking is the model where financial services are embedded directly into everyday apps and platforms, so a customer completes payments, lending, onboarding, and authentication without opening a separate bank channel. The institution becomes the trusted engine behind the experience rather than a destination you travel to.

For years the goal was simple digitisation, turning familiar banking services into apps, portals, and self-service screens. Invisible banking goes further. Those same services become native parts of the platforms people already trust, working as a quiet layer in the background of everyday life.

India's lead in embedded finance is not an accident. It rests on a digital foundation built deliberately over the last decade.

The Jan Dhan, Aadhaar, and Mobile trinity brought identity, access, and inclusion to a population scale [1]. India's digital public infrastructure added interoperable rails that let trust and innovation flow across the system. Platforms such as UPI, IMPS, and Bharat BillPay turned complex banking plumbing into instant, everyday utilities, with UPI alone now processing billions of transactions every month [2].

The scale of the shift is hard to overstate. The World Bank has noted that India reached its financial inclusion goals in about six years, a milestone that might otherwise have taken close to 47 years without this digital public infrastructure [1].

Newer consent-based frameworks like the Account Aggregator network [3] and the Open Credit Enablement Network are now extending that same foundation into data and credit.

Here is the part that rarely makes the headline. Every invisible transaction depends on something the customer never sees: Cryptography.

When a payment clears, an identity is verified, or financial data moves between a platform and a bank, encryption is what keeps it private and tamper-proof. As banking spreads across more platforms, fintechs, and rails, that cryptographic layer becomes the true load-bearing wall of the system.

Trust, in other words, is not a feeling. It is math running quietly in the background.

That math is now under pressure. Quantum computers, once they reach scale, will be able to break the public-key encryption that secures today's financial systems. The analyst firm Gartner expects conventional asymmetric cryptography to become unsafe by 2029 and fully breakable by 2034 [4].

The danger is not only in the future. Adversaries can harvest encrypted financial data today and store it, waiting to decrypt it later once a capable quantum machine arrives. Security researchers call this harvest-now, decrypt-later [5]. Financial data has a long shelf life, so KYC records, transaction histories, and account details captured this year could still be sensitive, and exposed, years from now. Banks are already responding, inventorying their cryptography and piloting quantum-safe alternatives as a multi-year priority rather than a distant concern [6].

This is why global standards bodies have already published post-quantum cryptography (PQC), a new generation of algorithms designed to resist quantum attacks [7].

Invisible banking calls for a matching principle in security: protection should be as embedded and quiet as the banking it guards, and quantum-safe by design.

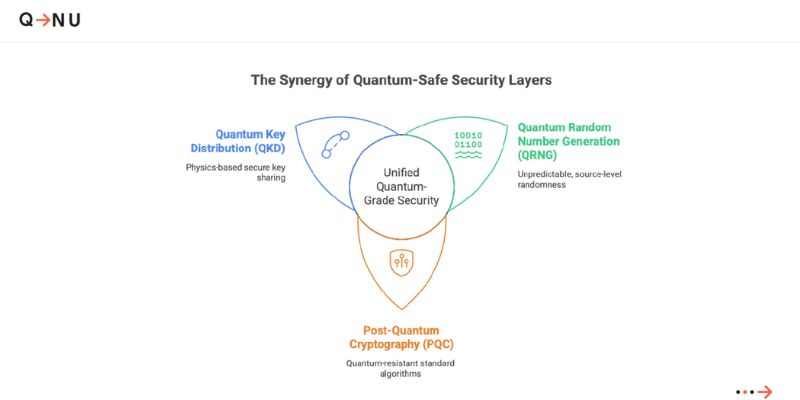

That principle sits at the core of our QShield platform, which brings quantum-grade security into one integrated system. Quantum key distribution (QKD) uses the laws of physics to share encryption keys that expose any attempt to intercept them. Quantum random number generation (QRNG) creates keys with no hidden pattern, secured right at the source. Post-quantum cryptography adds standard-compliant algorithms built to withstand quantum machines.

The World Economic Forum points to this same combination, QKD, QRNG, and post-quantum cryptography, as the foundation of quantum security for financial services [8].

Together they form a layer the customer never notices and an attacker cannot quietly break.

For a financial institution, this is where strategy meets security. The architecture of invisible banking, all those rails and integrations, only holds if the cryptography underneath it is sovereign, validated, and ready for the quantum era. Analysts at McKinsey note that leading banks are already combining post-quantum cryptography with quantum key distribution and prioritising crypto-agility to prepare for this shift [9].

That is the work we focus on for banking and finance, with quantum-safe deployments already running across banking, payments, and critical infrastructure. Our technology also operates at national scale, including India's first 1,000 km inter-city quantum key distribution network, independently certified by TEC and VIAVI Solutions. It is why MarketsandMarkets has recognised us as a global leader in quantum key distribution [10], and why, with 12+ granted patents and many more in the funnel, we hold India's largest quantum security IP portfolio.

Security is an immune system, built before the infection, never after.

Invisible banking may make the institution harder to see, but it makes trust more valuable than ever. The banks that lead will be the ones that pair regulatory credibility and rich customer experiences with security strong enough for what is coming. Forrester advises security leaders to begin their post-quantum migration now rather than wait for the threat to arrive [11].

The quiet revolution is here.

The real question for every financial institution is whether the engine running underneath it is ready.

Explore quantum-safe security for banking and finance and see what it takes to stay trusted in the quantum era.